Top 2024 UK Property Statistics [Freehold & Leasehold]

As of 2024, key property statistics reveal shifts in demand for freehold homes, largely driven by changing legislation around leasehold properties, as well as a push toward greater transparency in property dealings.

For buyers, these statistics offer valuable insights into market trends, helping them make informed decisions about property types. For sellers and investors, understanding these trends is vital to capitalising on opportunities in this ever-evolving market.

This article will focus on freehold and leasehold properties, analysing the latest trends and statistics to provide a comprehensive overview of their impact on the UK property market in 2024.

Key 2024 UK Property Statistics Overview

The UK property market in 2024 continues to present changing economic conditions, evolving buyer preferences, and significant developments in housing supply, while house prices have seen a modest yet steady growth.

This has been influenced by fluctuating interest rates, government housing policies, and a growing demand for affordable homes. Buyers are increasingly looking for stability, while investors remain cautious but optimistic, given the market’s resilience amidst economic challenges.

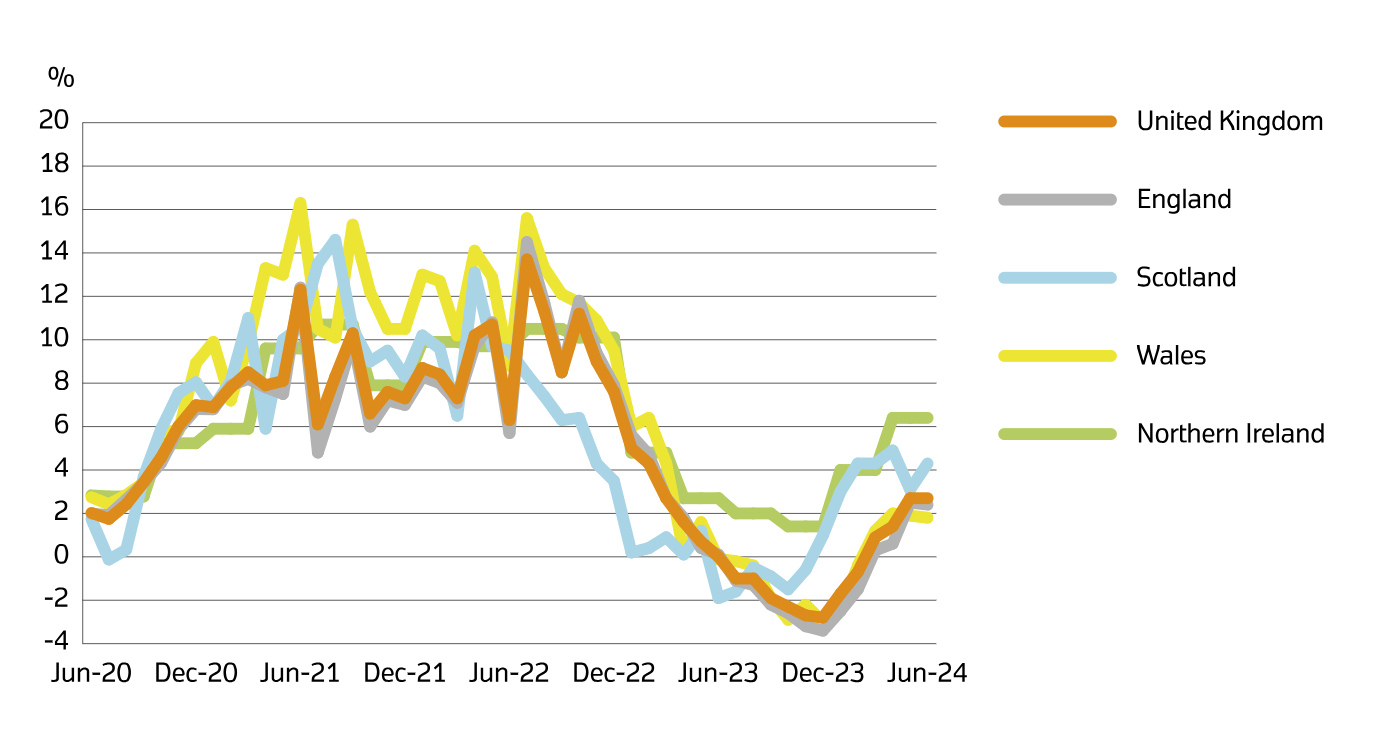

The UK House Price Index summary for 2024 states:

- Average UK house price annual inflation was 2.7% in the 12 months to June 2024.

- The average UK house price was £288,000 in June 2024 (provisional estimate)

- The average UK house price in June 2024 is £8,000 higher than 12 months ago.

- Compared to 2023, average house prices in the 12 months leading up to June 2024:

- Increased in England to £305,000 (2.4%)

- Increased in Wales to £216,000 (1.8%)

- Increased in Scotland to £192,000 (4.3%).

- Increased in Northern Ireland to £185,000 (6.4%).

‘Annual price change for UK by country over the past 5 years’, UK House Price Index, 2024

Analysis of Freehold Property Statistics

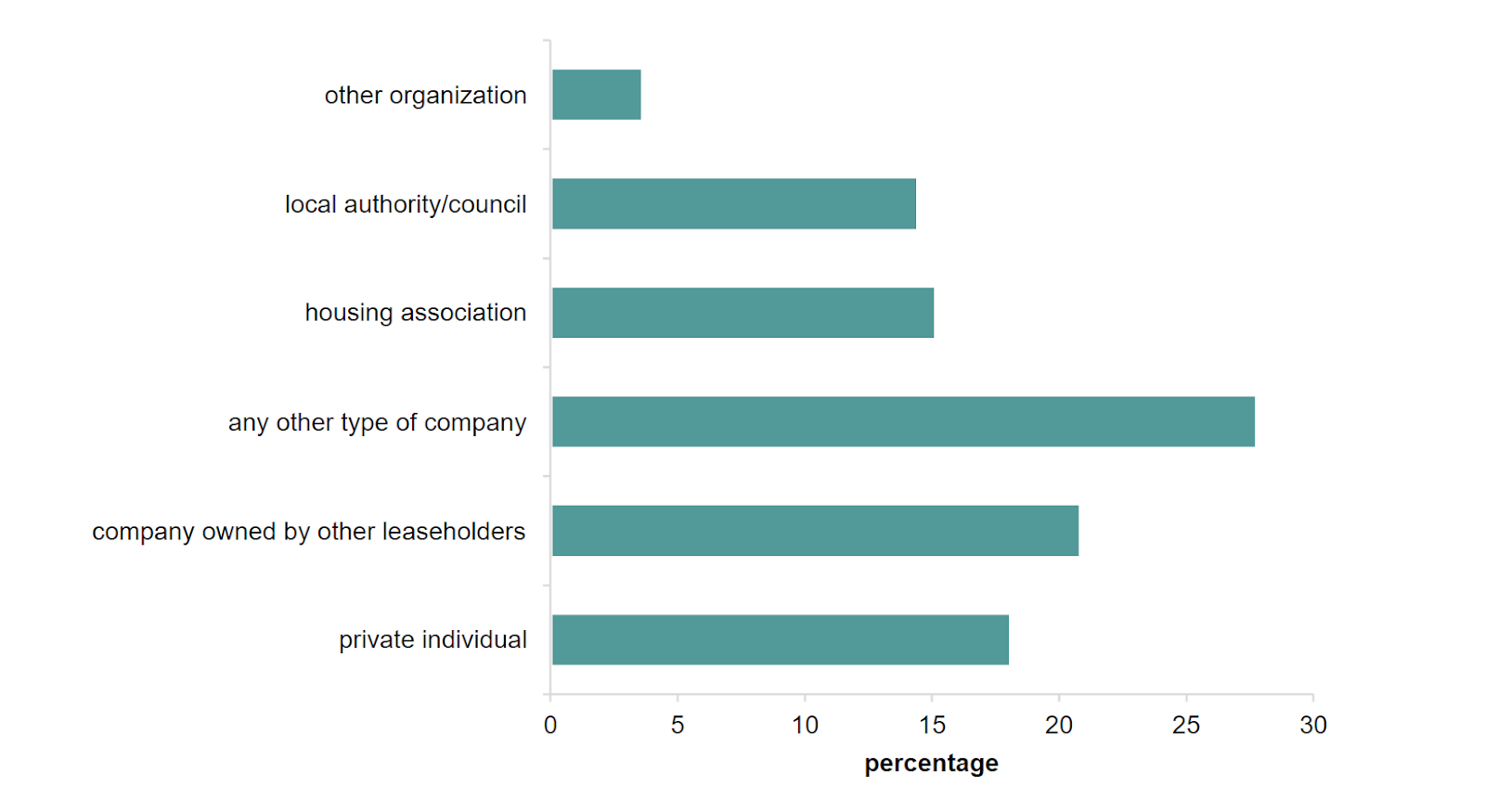

- In 2022, almost half of the freeholders of flats were Limited companies, owned by leaseholders (21%) or by unconnected individuals/businesses (28%). (GOV.UK)

- Other types of freeholders in the UK included private individuals (18%), housing associations (15%) and local authorities (14%). (GOV.UK)

- The remaining 4% were other organisations, such as churches or charities. (GOV.UK)

- In 2017, the most freehold properties were sold in: (ONS, via EvolutionProperties)

- Leeds, with 9,841 freehold transactions.

- Birmingham was second with 8,752 freehold properties.

- Cornwall ranked third with 8,726 freehold properties.

- County Durham ranked fourth with 7,255 freehold property sales.

‘Freehold ownership of leasehold flats’, GOV.UK, 2021-22

Analysis of Leasehold Property Statistics

- There are around 4.98 million leasehold homes in England, of which 70% are flats and 30% are houses. (House of Commons)

- The majority of flats in the private sector are leasehold (an estimated 94% of owner-occupied flats and 71% of privately rented flats). (House of Commons)

- Around 8% of houses in England are leasehold. (House of Commons)

- Out of around 207,000 transactions in total, 24% of residential property transactions in 2022 were leasehold. (House of Commons)

- Almost all flats were sold on a leasehold basis compared to 7% of houses. (House of Commons)

- The proportion of new-build houses sold as leasehold rose from 7% in 1995 to a peak of 15% in 2016, but significantly dropped to less than 1% by December 2022. (House of Commons)

- Leasehold properties account for around half of the sales in London and over four fifths (85%) of sales in Prime Central London. (SERC)

- Very short leases imply discount rates of around 5-6%, whereas long leases, close to 100 years left, imply discount rates between 3-4%. (SERC)

- At around 60 years, discount rates appear to flatten or even slightly increase. (SERC)

- More than a third of share of freehold flats have a lease term longer than 945 years. (SERC)

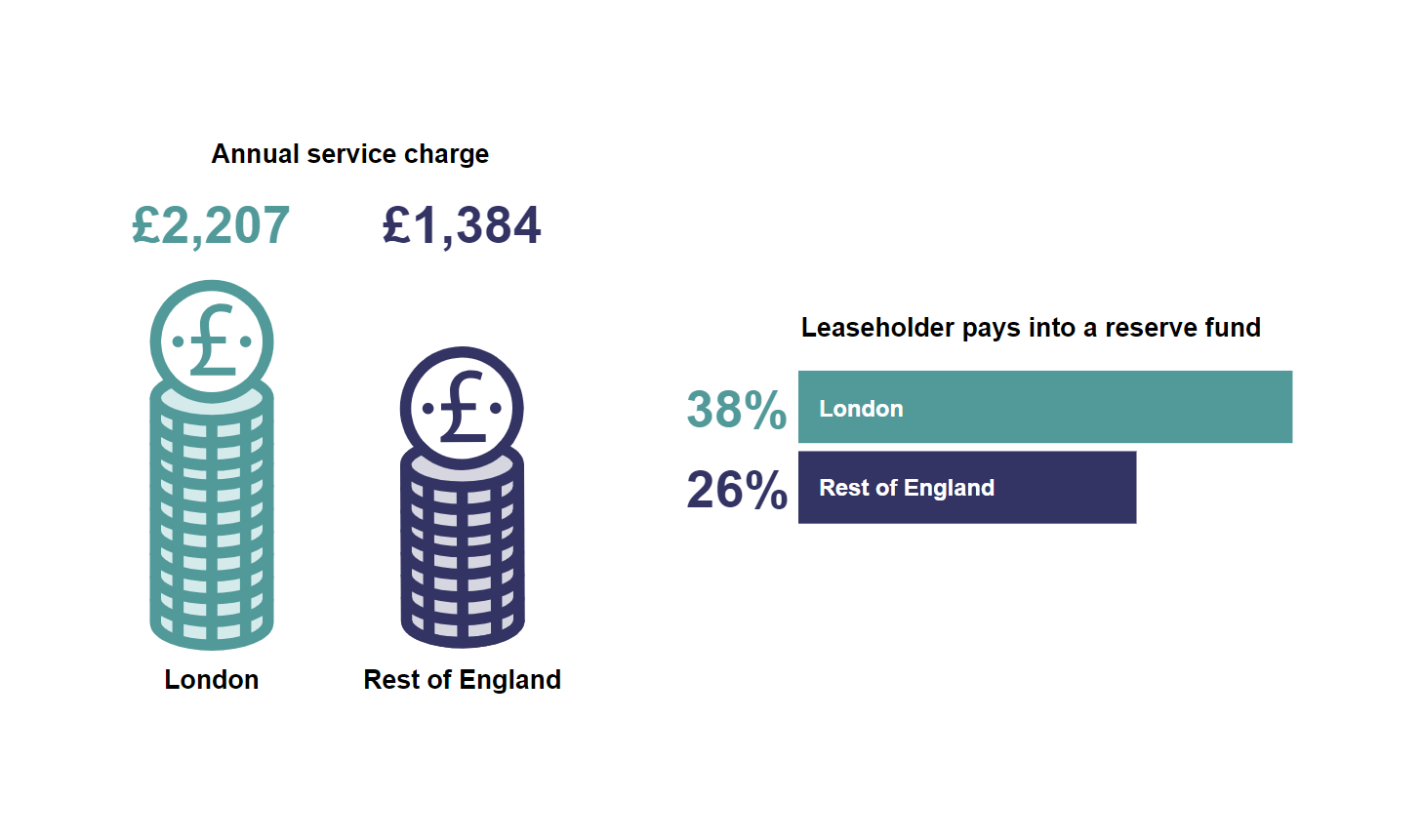

- Service charges are on average significantly higher in London, where leaseholders were also more likely to be paying into a reserve fund to cover repairs and maintenance.

‘Annual service charges of London vs rest of England’, House of Commons, 2024

Impact of Recent Legislation on Collective Property Ownership

In 2024, the UK property market continues to witness the ripple effects of recent legislative reforms, particularly those aimed at enhancing transparency and fairness in leasehold arrangements. One of the most significant developments is the ongoing push for leasehold reform, which has introduced a series of changes to empower leaseholders and encourage more equitable property ownership structures.

Among the reforms is the ground rent abolition for new leasehold properties, which came into effect in 2022 under the Leasehold Reform (Ground Rent) Act. This legislation effectively eliminates the practice of escalating ground rents for future leasehold agreements, which had been a major financial burden for leaseholders.

As a result, prospective buyers of new-build leasehold properties no longer face the uncertainty of increasing ground rents, making leasehold ownership more appealing for some.

Additionally, the government has expressed a strong commitment to simplifying the collective enfranchisement process, which allows leaseholders to collectively purchase the freehold of their property. Under proposed reforms, the process of buying out the freeholder is expected to become more streamlined and affordable, with potential caps on the costs of enfranchisement.

This move aims to grant greater control to leaseholders, particularly in shared residential blocks, fostering more collaborative ownership models. However, this could also lead to a gradual shift away from leasehold transactions as collective freehold ownership becomes more accessible.

Freeholder and Leaseholder Insights

The 2024 UK property statistics offer valuable insights into the evolving dynamics of freehold and leasehold properties, with implications for buyers and investors alike. For prospective homeowners, understanding these trends is key to making informed decisions that align with long-term financial goals.

For Freeholders

Freehold properties have long been regarded as the gold standard in property ownership due to the complete control they offer over both the building and the land it sits on. The latest statistics show a growing demand for freehold homes, driven in part by the ongoing leasehold reforms.

For buyers, this translates into increased long-term value and ownership freedom, as freehold properties do not carry the same restrictions or fees often associated with leasehold arrangements, such as ground rent or service charges.

Freehold properties, especially in regions like Leeds and Birmingham, have seen high transaction volumes, indicating a solid demand. For buyers seeking stability, this suggests that freehold homes in these areas are likely to retain or even grow in value over time.

Furthermore, freehold properties provide the owner with the flexibility to make modifications without needing permission from a freeholder, making them ideal for buyers looking for long-term investment potential and greater autonomy.

Tips for freehold buyers: Look for properties in regions with high freehold transaction volumes, as these may offer stronger investment opportunities. Consider the potential for capital growth in areas like Leeds and Birmingham, where freehold demand has been consistently high.

For Leaseholders

Leasehold properties, while still prevalent, particularly in cities like London where space is at a premium, require careful consideration. Leaseholders typically have the property for a set number of years, as specified in the lease, but down own the land it sits on. As such, buyers must evaluate lease terms, which can significantly affect a property’s long-term value.

A key factor is the remaining length of the lease—properties with leases of fewer than 100 years often require costly extensions, which can diminish the appeal for buyers and investors.

Additionally, potential buyers should account for ongoing costs, such as ground rent (for older properties) and service charges. The statistics highlight that service charges in London, in particular, can be significantly higher than in other parts of the country, which may affect the overall affordability of a property.

It’s also crucial for leasehold buyers to be aware of their statutory rights, such as the right to extend the lease or collectively purchase the freehold, as these can offer pathways to greater control over their property.

Tips for leasehold buyers: Pay close attention to lease terms and the associated costs of extending leases, particularly for properties with shorter leases. Investigate service charges and the potential for rising fees, especially in city centres. Understanding your rights as a leaseholder can provide leverage in negotiations and help mitigate future costs.

Closing Thoughts

In summary, while freehold properties offer long-term security and freedom, leasehold buyers must navigate more complexities. Both groups can use the latest data to make more strategic purchasing decisions, balancing immediate costs with long-term value.

Looking to collectively purchase your freehold? Use our freehold purchase calculator today for an instant estimate on the premium of your freehold.